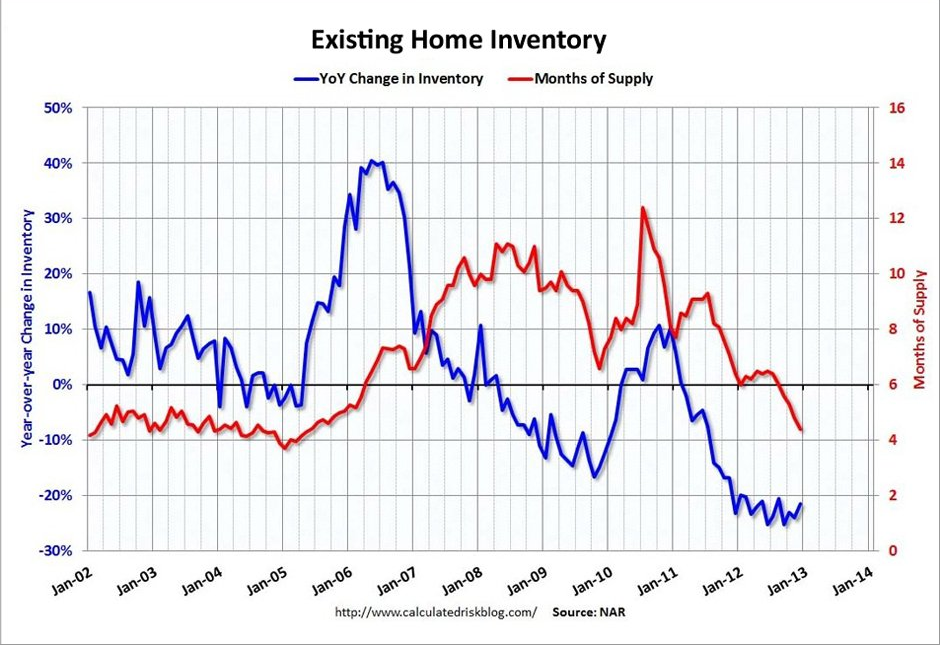

Today’s existing home sales number was a little weaker than expected.

Today’s existing home sales number was a little weaker than expected.

But have no fear, the housing comeback train continues.

Calculated Risk shows the number of months worth of existing home supply (red line). And that number continues to drop.

Which means: The price of your home is going to go up, as inventory gets tighter.