There has been a lot written about millennials and their preference to live in city centers above their favorite pizza place. Some have even gone so far as to say that millennials are a “Renter-Generation”.

And while this might be true for some millennials, more and more research has surfaced that shows for the vast majority, owning a home is a major part of their American Dream!

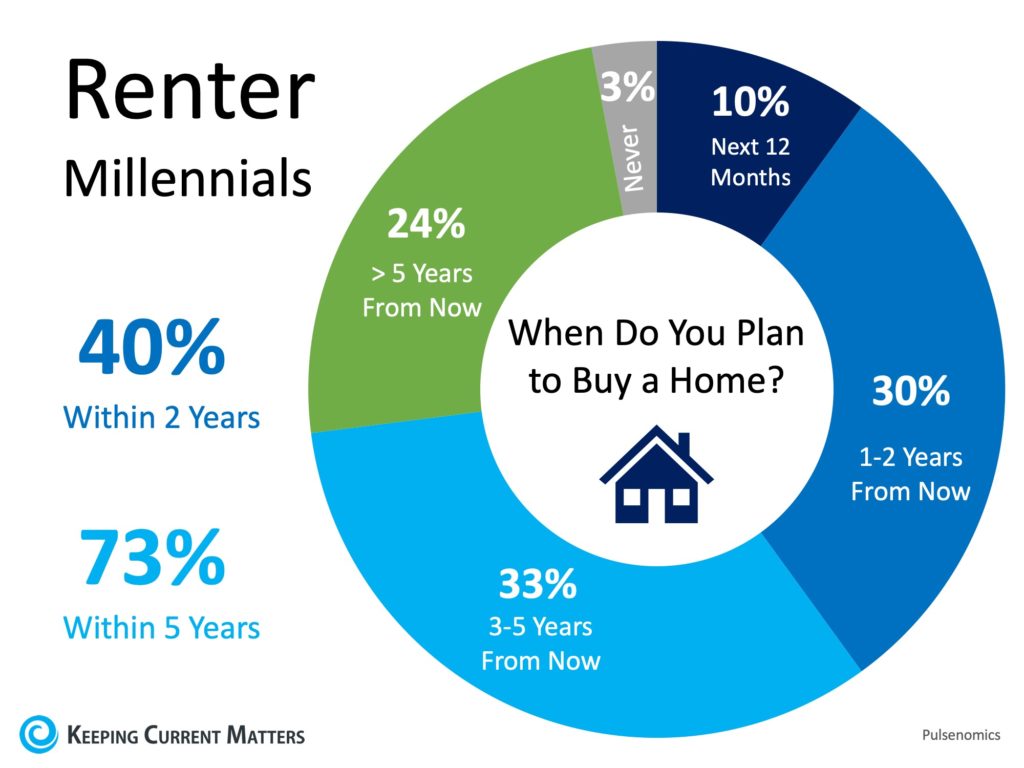

New research shows that 66% of millennials who currently rent are determined to buy a home! Seventy-three percent of those surveyed by Pulsenomics plan to buy a home in the next five years, with 40% planning to do so within the next two years!

“Millennials want to own a home as much as prior generations,” Ali Wolf, Director of Economic Research at Meyers Research says. “We saw millennial shoppers scooping up homes in 2018—and 2019 will be no different.”

Bottom Line

Are you one of the millions of renters who are ready and willing to buy a home? Meet with a local real estate professional who can help determine your ability to buy now!