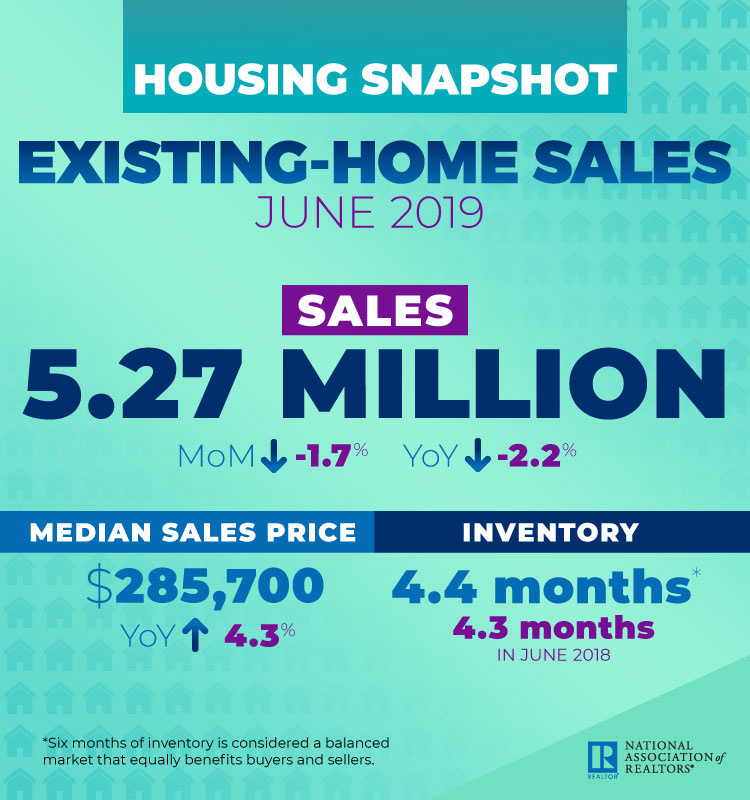

Despite mortgage rates dipping below 4%, more jobs filled than ever before, and record-high consumer net worth, existing-home sales turned south in June, running at a pace similar to 2015 levels, the National Association of REALTORS® reported Tuesday. While economic indicators portend a strong housing market, low supply on the lower end—which leaves first-time homebuyers with few options—is helping to hold sales back, NAR Chief Economist Lawrence Yun says.

Total existing-home sales, comprising transactions for single-family homes, townhomes, condos, and co-ops, dropped 1.7% month over month in June to a seasonally adjusted annual rate of 5.27 million, according to NAR. Sales are down 2.2% from a year ago. Two of the four major U.S. regions, the Northeast and Midwest, recorded minor sales increases last month, while the South and West posted larger declines. “Imbalance persists for mid- to lower-priced homes, with solid demand and insufficient supply, which is consequently pushing up home prices,” Yun says.

The median existing-home price for all housing types reached a record high of $285,700 in June, up 4.3% from a year ago.

Yun says other factors besides high home prices and inventory shortages may also make buyers skittish. “Either a strong pent-up demand will show in the upcoming months, or there is a lack of confidence that is keeping buyers from this major expenditure,” Yun says. “It’s too soon to know how much of a pullback is related to the reduction in the homeowner tax incentive.”

Here’s a closer look at more key indicators in the housing market in June from NAR’s latest report:

- Inventory: Total housing inventory rose to 1.93 million in June, up from 1.91 million in May. But the June figure is unchanged from inventory levels a year ago. Unsold inventory is at a 4.4-month supply at the current sales pace.

- Days on the market: Fifty-six percent of homes sold in June were on the market for less than a month. Properties typically remained on the market for 27 days in June, up slightly from 26 days a year ago.

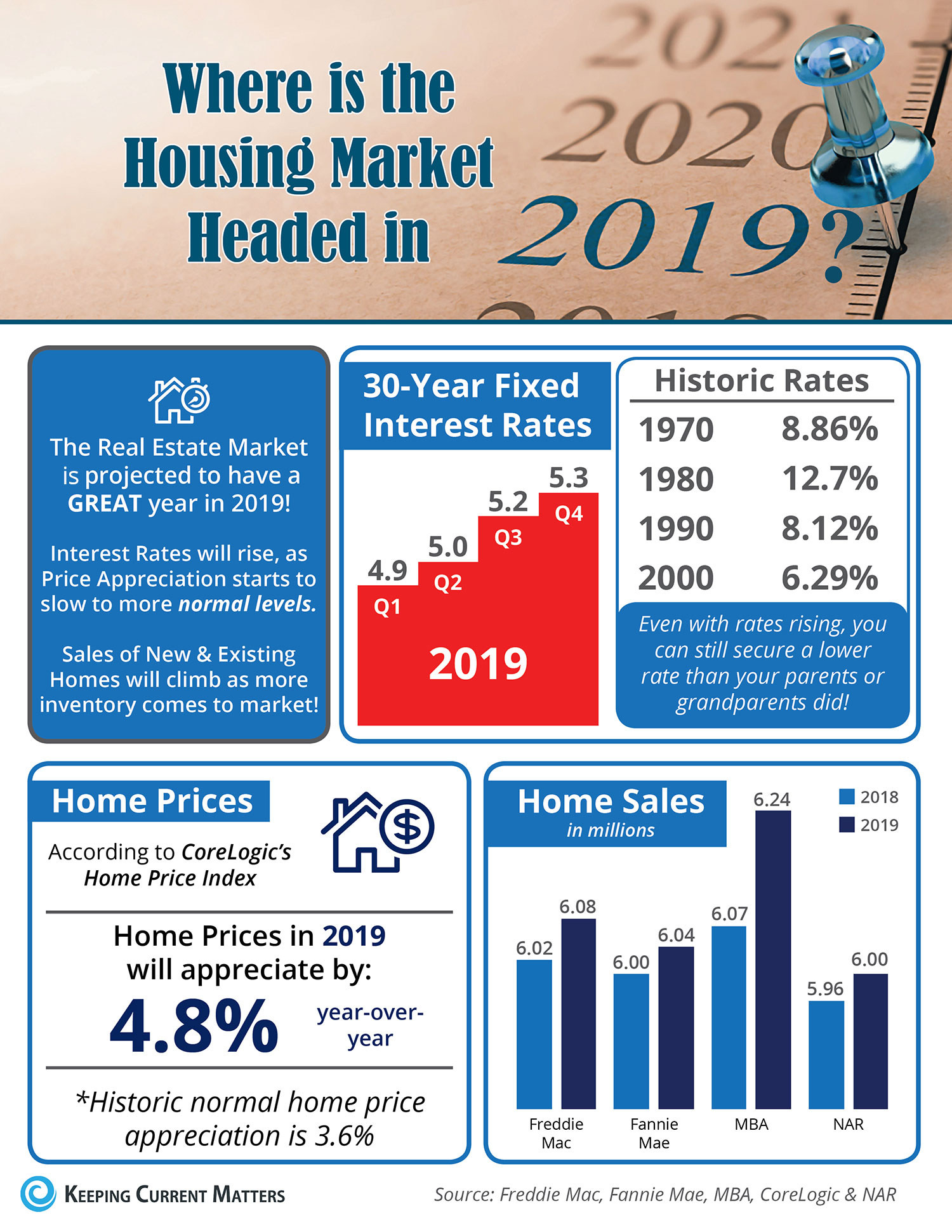

- Mortgage rates: The 30-year fixed-rate mortgage dropped to 3.80% in June, down from 4.07% in May, according to Freddie Mac. “Historically, these rates are incredibly attractive,” says NAR President John Smaby. “Securing and locking in a mortgage now—given the current favorable conditions—is a decision that will pay off for years to come.”

- First-time buyers: First-time buyers comprised 35% of sales in June, up from 31% a year ago.

- All-cash sales: Sixteen percent of transactions in June were paid in cash, down from 22% a year ago. Individual investors, who account for the bulk of cash sales, purchased 10% of homes in June, down from 13% a year ago.

![A 44-Point SEO Checklist to Help Improve Your Process [Infographic]](http://www.emmanuelfonte.com/wp-content/uploads/2023/08/SEO-678x226.png)