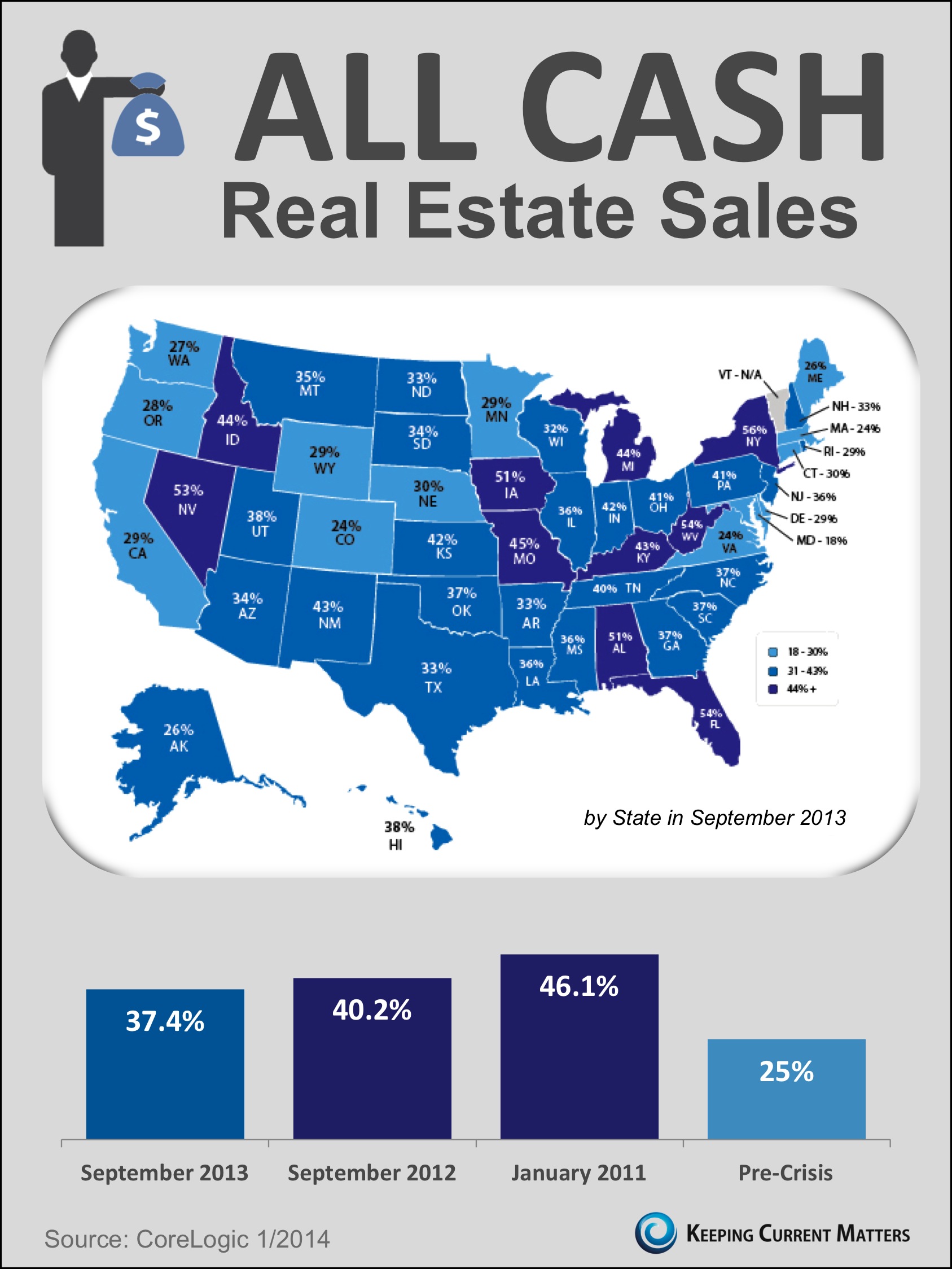

Courtesy of the great folks at KCM.

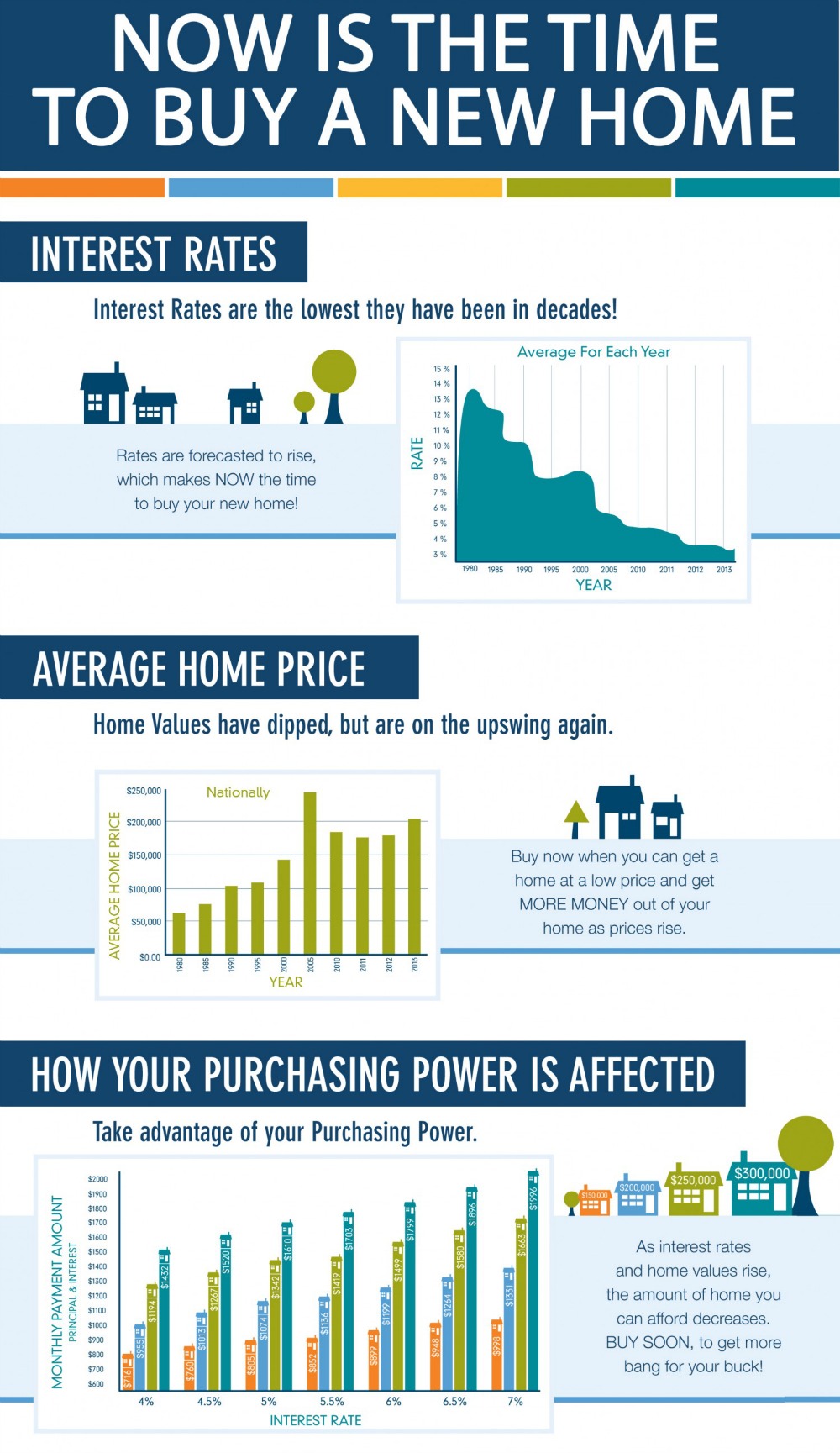

Courtesy of the great folks at KCM.

Emmanuel Fonte | Music | Art | Leadership

If music be the food of love, play on. Emmanuel Fonte website is about music, art, real estate, architecture, design and decor. Occasionally, I talk about my other passion, hockey.

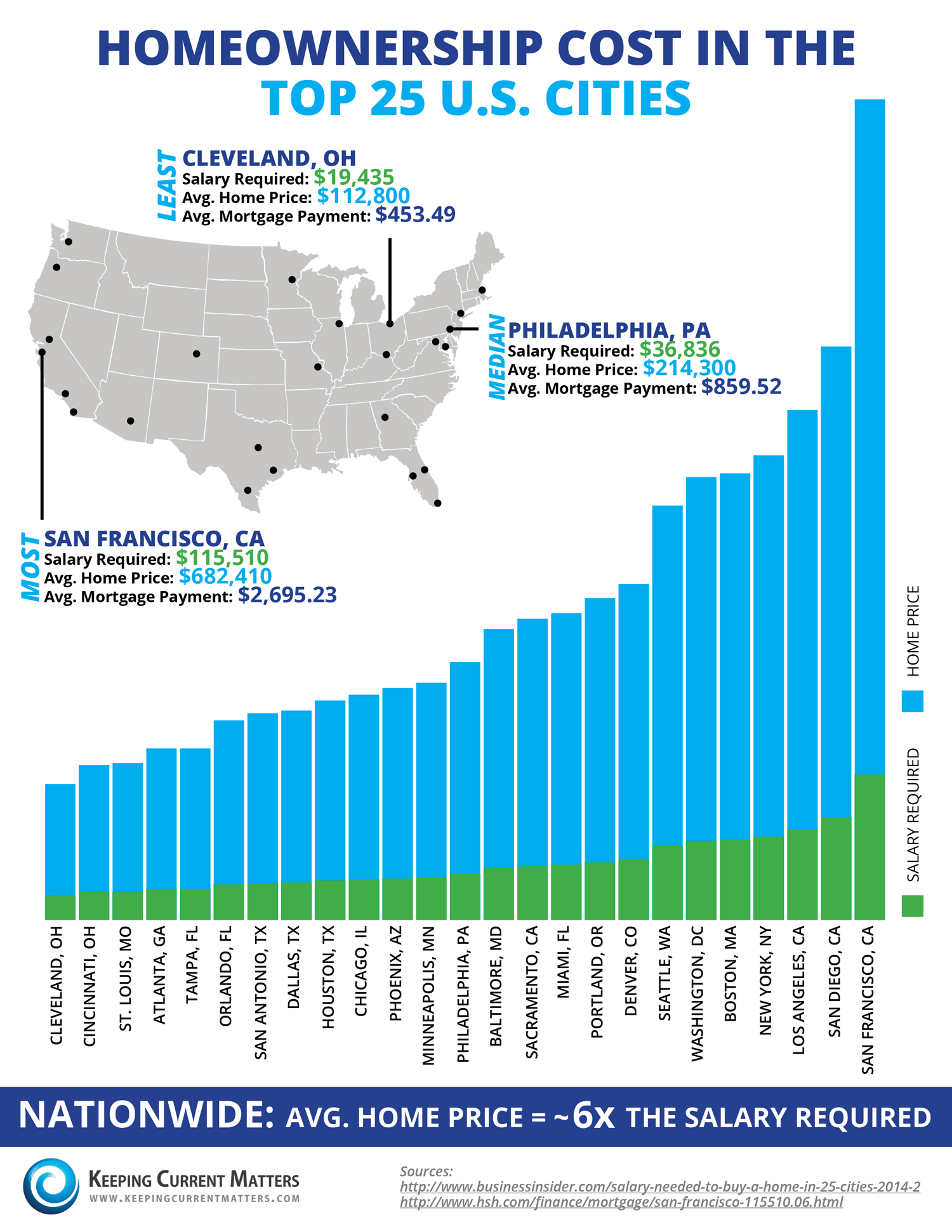

Courtesy of the great folks at KCM.

An interesting look at what 1% savings on your mortgage could be used for.

Even better than being pre-approved is Certified Mortgage ReadyTM, something that we at John L. Scott can help home buyers with. It allows borrowers to compete with cash offers.

Energy tax credits on select improvements available through the end of tax year 2013.

Energy tax credits on select improvements available through the end of tax year 2013.

If you upgraded one or more of the following systems last year, you may be eligible to take a tax credit — up to $500 — on your return.

The energy tax credits are small, but at least a credit is better than a deduction:

Limits on IRS energy tax credits besides $500 max

Certain systems capped below $500

No matter how much you spend on some approved items, you’ll never get the $500 credit — though you could combine some of these:

| System | Cap |

| New windows | $200 max (and no, not per window—overall) |

| Advanced main air-circulating fan | $50 max |

| Qualified natural gas, propane, or oil furnace or hot water boiler | $150 max |

| Approved electric and geothermal heat pumps; central air-conditioning systems; and natural gas, propane, or oil water heaters | $300 max |

And not all products are created equal in the feds’ eyes. Improvements have to meet IRS energy-efficiency standards to qualify for the tax credit. In the case of boilers and furnaces, they have to meet the 95 AFUE standard. EnergyStar.gov has the details.

Tax credits cover installation — sometimes

Rule of thumb: If installation is either particularly difficult or critical to safe functioning, the credit will cover labor. Otherwise, not. (Yes, you’d have to be pretty handy to install your own windows and roof, but the feds put these squarely in the “not covered” category.)

Installation covered for:

Installation not covered for:

How to claim the energy tax credit

This article provides general information about tax laws and consequences, but isn’t intended to be relied upon as tax or legal advice applicable to particular transactions or circumstances. Consult a tax professional for such advice, and remember that tax laws may vary by jurisdiction.

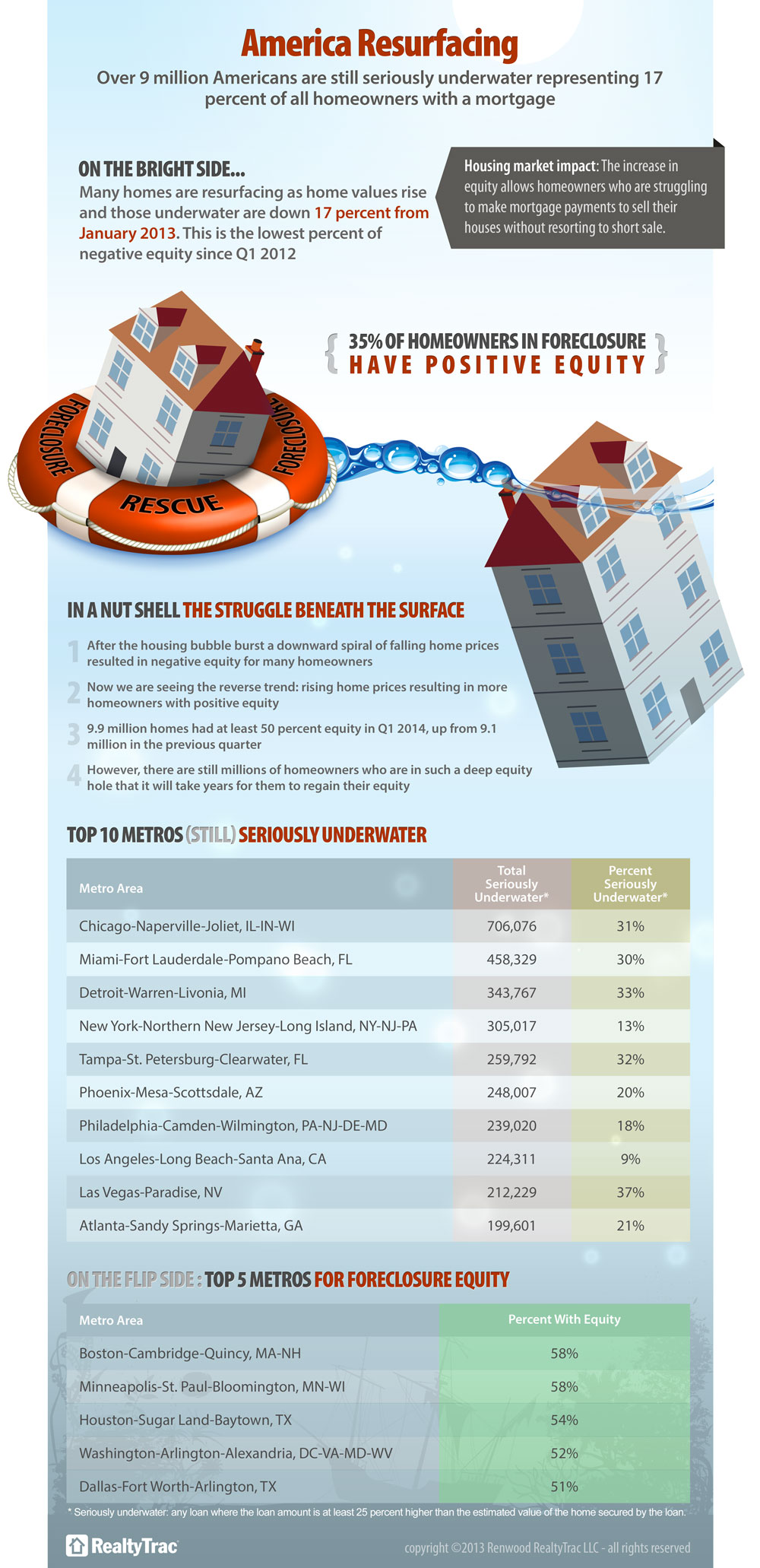

An interesting infographic via Trulia.

VA loans are the most misunderstood mortgage program in America. Industry professionals and consumers often receive incorrect data when they inquire about them. In fact, misconceptions about the government guaranteed home loan program are so prevalent that a recent VA survey found that approximately half of all military veterans do not understand it.

VA loans are the most misunderstood mortgage program in America. Industry professionals and consumers often receive incorrect data when they inquire about them. In fact, misconceptions about the government guaranteed home loan program are so prevalent that a recent VA survey found that approximately half of all military veterans do not understand it.

With this in mind, we would like to debunk the most common myths about VA Loans.

Fact: Veterans and active duty military can use the VA loan many times. There is a limit to the borrower’s entitlement. The entitlement is the amount of loan the VA will guarantee. If the borrower exceeds their entitlement, they may have to make a down payment. Never the less, there are no limitations on how many times a Veteran or Active Duty Service Member can get a VA loan.

Fact: For eligible participants, VA mortgage benefits never expire. This myth stems from confusion over the veteran benefit for education. Typically, the Montgomery GI Bill benefits expire 10 years after discharge.

Fact: You can have two (or more) VA loans out at the same time as long as you have not exceeded your maximum entitlement and eligibility. In order to have more than one VA loan, the borrower must be able to afford both payments and sufficient entitlement is required. If the borrower exceeds their entitlement, they may be required to make a down payment.

Fact: By law, homeowners with VA loans may rent out their home. If the home is located in a non-rental subdivision, the VA will not guarantee the loan. If the home is located in a subdivision (such as a co-op) where the other owners can deny or approve a tenant, the VA will not approve the financing. When an individual applies for a VA loan, they certify that they intend on making the home their primary residence. Borrowers cannot use their VA benefits to buy property for rental purposes except if they are using their benefits to buy a duplex, triplex or fourplex. Under these circumstances, the borrower must certify that they will occupy one of the units.

Fact: If a borrower has a claim on their entitlement, they will still be able to get another VA loan, but the maximum amount they would otherwise qualify for may be less. For example, Mr. Smith had a home with a $100,000 VA loan that foreclosed in 2012. If Mr. Smith buys a home in a low cost area, he will have enough remaining eligibility for a $317,000 purchase with $0 money down. If he did not have the foreclosure, he would have been able to obtain another VA loan up to $417,000 with no money down payment.

Veterans and Active duty military deserve affordable home ownership. In recent years, the VA loan made up roughly 13% of all home purchase financing. This program remains underused largely because of misinformation. By separating facts from myth, more of America’s military would be able to realize their own American Dream.

Phil Georgiades is our guest blogger today. Phil is the Chief Loan Steward for VA Home Loan Centers, a veteran and active duty military services organization.