click image to interact.

Mortgage rates are still at near-record lows, with 30-year fixed-rate loans averaging 4.09% (with an average 0.7 point) for the week ending Sept. 22, 2011, while 5/1 ARMs averaged 3.02% with an average 0.6 point, according to Freddie Mac. And many American homeowners are hoping to take advantage of those rates by applying to refinance their mortgages. In fact, the vast majority of recent mortgage applications have been applications to refinance: 78% for the week ending Sept. 16, 2011, according to the Mortgage Bankers Association.

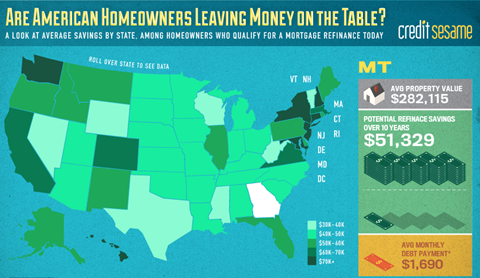

That’s why it may come as a surprise that many homeowners are still not taking advantage of those savings opportunities. And we’re not talking about those who do not qualify to refinance (the 23% of homeowners with a mortgage who owe more to the bank than their properties are worth, for example). Credit Sesame recently analyzed data from its user base and found out that, on average, homeowners who would qualify for a refinance based on their credit profiles, income and the equity in their homes, are foregoing thousands of dollars in savings over a 10-year period: from an average of $38,387 in Nevada to an average of $97,170 in New Jersey.

In this interactive infographic, based on Credit Sesame data, we show you the average savings homeowners could reap over a 10-year period if they refinanced their mortgages, as well as average property values and homeowners’ average monthly debt payments (including mortgage, car and student loans, credit card debt, and home equity loans or lines of credit).

Speak Your Mind

You must be logged in to post a comment.