In recent years, real estate has become something of a polarizing topic; there are those who argue that it’s still a worthy long-term investment with tangible benefits; and others who don’t see the value of owning a home, financial or otherwise. Regardless of which side of the argument you come out on, housing is a major part of our national economy. Furthermore, people are always going to need a place to live, so it’s a worthy discussion to be had.

In recent years, real estate has become something of a polarizing topic; there are those who argue that it’s still a worthy long-term investment with tangible benefits; and others who don’t see the value of owning a home, financial or otherwise. Regardless of which side of the argument you come out on, housing is a major part of our national economy. Furthermore, people are always going to need a place to live, so it’s a worthy discussion to be had.

There are a number of catch phrases that have become quite popular amongst real estate agents and media alike, such as “now is the time to buy” and “it’s a buyer’s market”. For some people, right now is a great time to buy a home, but for others, it’s not. The point is that buying a home is a personal decision based on each buyer’s unique circumstances. There’s no “one size fits all” model when it comes to real estate, so the best you can do is arm yourself with the right information so you can make the best decision for you.

With this in mind, we thought it might be interesting to compare today’s real estate market with that of 2006 when housing was at its peak. Five years ago, home values were soaring, sales were frenzied, and home ownership was at an all-time high. Inventory levels simply could not keep up with demand, so bidding wars were commonplace and homes flew off the market in record time.

With this in mind, we thought it might be interesting to compare today’s real estate market with that of 2006 when housing was at its peak. Five years ago, home values were soaring, sales were frenzied, and home ownership was at an all-time high. Inventory levels simply could not keep up with demand, so bidding wars were commonplace and homes flew off the market in record time.

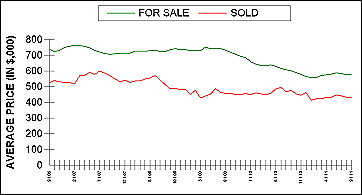

Today’s market is very different. It’s important to remember that all real estate is local, so markets can vary greatly – even within a single city – but there are some general trends that we’re seeing across the board. The first is home prices; very few areas were spared from the effects of declining prices. Inventory levels in recent years have also been higher than they were in 2006 and the average amount of time that it takes to sell a home is longer. All of this points towards this being a buyer’s market. Other buyer advantages include historically low interest rates and strong affordability. With this in mind, here are some interesting stats to consider:

- The average interest rate on a 30-year-mortgage today is 4.13%(2) and in September 2006 it was 6.41%(2)

- A $400,000 house today would have cost $642,650 in September 2006(1) which is a difference of $242,650. *The following scenarios assume these home prices.

- Using the above home prices and interest rates, the monthly payment today would be $1,939.76 and in September 2006 it would have been $4,024.02 – a difference of $2,084.26 per month.

- The $2,084.26 per month savings adds up to a total of $750,333 when multiplied over the term of a 30-year loan.

- If today’s buyer took out a 30-year-loan at the current interest rate (4.13%), but made the same monthly payments as the buyer in 2006 ($4,024.02), the loan would be paid off in just over 10 years – the buyer in 2006 would still have almost 15 more years of payments.

1) calculated using FHFA figures for the West Coast in September 2011

2) from FHLMC website for September 2011

The math above is compelling, especially when you consider how much money is saved on compound interest over the life of a 30-year loan for the same home. But regardless of what the numbers show, buying a home is much more than a financial decision, it is one that is personal and should be reflective of each individual’s needs and circumstances. Unfortunately, we don’t have a crystal ball and cannot predict what interest rates are going to do or how the market is going to grow and change, but we do know people will always need a place to call home – and as long as that is the case – we will be here to help them.

The math above is compelling, especially when you consider how much money is saved on compound interest over the life of a 30-year loan for the same home. But regardless of what the numbers show, buying a home is much more than a financial decision, it is one that is personal and should be reflective of each individual’s needs and circumstances. Unfortunately, we don’t have a crystal ball and cannot predict what interest rates are going to do or how the market is going to grow and change, but we do know people will always need a place to call home – and as long as that is the case – we will be here to help them.

If you are interested in how this market affects you and your choices, please call me at 206-713-3244 or email Emmanuel@EmmanuelFonte.com

Speak Your Mind

You must be logged in to post a comment.